Your options when leaving

What you need now can seem more important than what you might need in the future. Making use of the relevant information, support and advice available to you makes it easier to reach your shorter-term and longer-term goals.

What you need now can seem more important than what you might need in the future. Making use of the relevant information, support and advice available to you makes it easier to reach your shorter-term and longer-term goals.

You can keep your money invested.

To help you keep your savings invested, find out more about the options you have when you leave your employer by:

If you’d like to keep your retirement savings invested for your future self to reduce the risk of not having enough to live on after you retire, these are your options.

Tip!

Keep your retirement savings invested in your savings pot instead of withdrawing this money in cash so that you can use it to buy a pension that you can live on one day when you are no longer

working.

Speak to a licensed financial adviser on 0860 000 381 or email mymoneymatters. Find out what you can do with your savings and what the tax implications are.

Email them a link with important information that will help them through the decisions they will need to make when it comes to their retirement savings and changing employers.

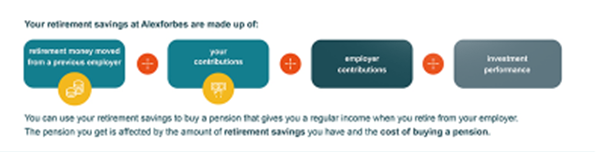

When you’re no longer earning a salary at the end of your working life, you can use your savings in your retirement fund to buy a pension that will give you regular income. Your employer has provided you with a provident or pension fund.

How does a retirement fund work?

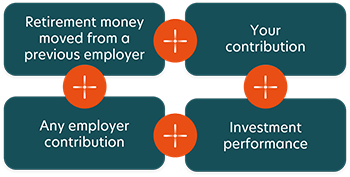

How much your pension will be depends on:

A benefit statement shows:

Here’s an explanation of your benefit statement.

View your benefit statement by registering on AF Connect. Your benefit statement will tell you how much you’ve saved and which portfolios your savings are invested in. You can also download the AF app on the Apple App Store or the Google Play Store.

With the new two-pot system, you can withdraw cash from your savings pot once in every tax year (1 March to 28 February). If you’ve made a withdrawal from your savings pot during the tax year, you won’t be allowed to make another cash withdrawal from your savings pot when you leave your employer. Although, if you have a small amount in your savings pot, you may be allowed to withdraw it. Withdrawing from your savings pot is taxed at your marginal tax rate – the same rate of tax you pay on your salary.

Remember, during your lifetime, you can take a total of R550 000 of your retirement savings tax free on retirement. However, all amounts you withdraw in cash (exceeding R27 500) before retirement will reduce this amount. How much you are taxed depends on how much you take and when you take it.

SARS sets the amount of tax you pay on any amount you withdraw. This can change from time to time. The latest information is available on SARS’ website. A financial adviser can help you work out how much tax you may need to pay if you plan on withdrawing any of your retirement savings in cash when you leave your job.

If you decide to withdraw any of your retirement savings in cash if you are retrenched, you may have to pay tax. SARS sets the amount of tax you pay on any amount you withdraw, depending on how your employer has classified your retrenchment. The rate of tax you must pay changes from time to time. This information is available on SARS’ website. A financial adviser can help you work out how much tax you may need to pay if you plan on withdrawing any of your retirement savings in cash when you have been retrenched.

It is especially important to have the support of a financial adviser if you have been retrenched, especially if you don’t find another job straight away or think you’ll struggle to cope financially. A financial adviser can help you make the most of what you have and try to keep as much of your retirement savings invested for your future self at the same time.

My retirement savings will stay invested so that they can carry on growing.

It is very important for you to keep your contact and other details up to date with Alexforbes so that you can keep receiving information about your retirement savings.

Please get in touch with the Client Contact Centre to update your details.