Retiring soon

Preparing to make decisions will give you the best chance of having enough to live on in retirement. It’s also important that you keep playing an active role in your money matters after you leave your employer.

If you’re only a few months away from retirement – invest in this time so that it is time well spent.

If you haven’t already, now is the time to connect with a financial adviser who can partner with you through the transition from being paid a salary to receiving an income in retirement.

Get startedPreparing to make decisions will give you the best chance of having enough to live on in retirement. It’s also important that you keep playing an active role in your money matters after you leave your employer.

The information on this site is designed to help you make informed decisions, as you get ready to retire. Once they’re informed, many people need or rely on a financial adviser to help them make the choices that are right for them based on their personal circumstances.

Email them a link to share this information that will also help them with the decisions they need to make about their retirement savings, as they prepare to retire.

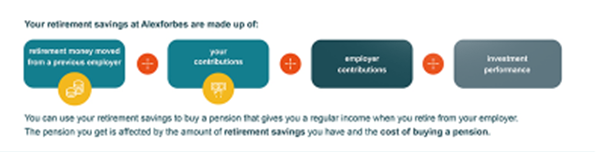

When you’re no longer earning a salary at the end of your working life, you can use your savings in your retirement fund to buy a pension that will give you regular income. Your employer has provided you with a provident or pension fund.

How does a retirement fund work?

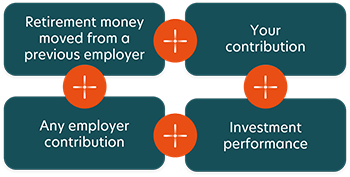

How much your pension will be depends on:

A benefit statement shows:

Here’s an explanation of your benefit statement.

View your benefit statement by registering on AF Connect. Your benefit statement will tell you how much you’ve saved and which portfolios your savings are invested in. You can also download the AF app on the Apple App Store or the Google Play Store.

If you’re closer to retirement, make contact with a financial adviser as soon as you can. We recommend that you start discussing your retirement plans with a financial adviser at least five years before your fund's normal retirement date.

You can retire early on the grounds of ill-health, if you:

The benefit you get will be the value of your retirement savings in the fund.

The age you must retire is determined by the rules of your retirement fund. However, if you don’t need to start receiving a pension right away (for example, if you are able to continue working on a contract basis), you can keep your retirement savings invested in the fund until you’re ready to buy a pension. This is called delaying or deferring retirement. Your financial adviser can explain which of your retirement fund benefits will stop if you choose this option. Find out more about delaying retirement here.

A financial adviser can help you to make a financial decision that is right for you based on your individual circumstances. Financial advisers charge fees that are based on the financial products they help you select. For example, if a financial adviser helps you to use your retirement savings to buy a flexible pension or a guaranteed pension, you will be charged a fee.

Fees can be charged up front when you buy a pension and on an ongoing basis if you choose to receive ongoing advice. The up-front fee a financial adviser charges is limited to 1.5% + Vat of the amount you use to buy a pension, but the actual amount is negotiated between you and your financial adviser. The fees are usually deducted from the amount you use to buy a pension.

Please contact our My Money Matters Centre, where you can receive retirement benefit counselling and advice from our qualified financial consultants.

After retiring, you may experience a delay in receiving income for the first month due to administrative processes. This is because administrators wait until your last fund contribution is received and invested.

This is where the money in your savings pot comes in very handy. You can withdraw the money you need a few months before your retirement date. Otherwise, financial advisers suggest setting aside your leave payout, or using a credit card. It’s also good to notify creditors of potential delays in payments because if you don’t have savings, the process can take six to eight weeks.

It’s a good idea to start the process at least three months before you retire.

Your retirement savings can be divided between flexible pensions (living annuities) and guaranteed pensions (life annuities). There may be up-front and ongoing fees but the amounts will differ depending on the type of pension you choose and what is agreed on by you and your financial adviser.

In the case of a flexible pension, there will be investment fees on your investment portfolios. Investment portfolio fees are deducted from the value of your investments and won’t be shown separately on your statements. An administration fee is also charged for the administration involved to pay your pension to you and for preparing and submitting your tax information.

You don’t have to pay tax on the first R550 000 you withdraw in cash from your retirement savings. The tax-free amount depends on how much cash you’ve taken from your retirement savings in the past. Some people choose to only take the tax-free portion at retirement but you can consider taking more if this extra cash can help you structure your income in the future. Depending on your income needs, you could save tax over a longer period of time (like five to ten years or more) by paying some tax now.

If you have a larger amount to invest, it can be worthwhile setting up more than one flexible income stream with the same service provider. In the future, you may want to convert from a flexible retirement income to a guaranteed retirement income. Remember, each flexible retirement income stream can be converted individually.