Options when starting a new job

Starting a new job is a big change. You may need some help to make good decisions as you start your new job.

Starting a new job is a big change. You may need some help to make good decisions as you start your new job.

To help you decide, find out more about your options by

If you’d like to keep your retirement savings invested for your future self to reduce the risk of not having enough to live on after you retire, these are your options.

Tip!

Keep your retirement savings invested for their real purpose - to provide you with income when you're no longer working. Avoid withdrawing cash from your savings pot during the year and when you change jobs.

Share this information with them. It will help them through the decisions they will need to make when it comes to their retirement savings and changing employers.

When you’re no longer earning a salary at the end of your working life, you can use your savings in your retirement fund to buy a pension that will give you regular income. Your employer has provided you with a provident or pension fund.

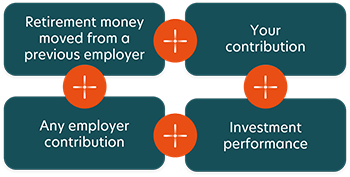

How does a retirement fund work?

How much your pension will be depends on:

A benefit statement shows:

Here’s an explanation of your benefit statement.

View your benefit statement by registering on AF Connect. Your benefit statement will tell you how much you’ve saved and which portfolios your savings are invested in. You can also download the AF app on the Apple App Store or the Google Play Store.

The rules of your fund will tell you if you can make extra contributions to your retirement savings in addition to your monthly contributions. These are called ‘additional voluntary contributions’. It is very important to contribute as much as you can every month.

You can choose a contribution amount from the options that are provided in the rules of your fund. It is very important to contribute as much as you can every month. You can find out more about your contribution options in your member booklet (which you can get from your HR department).

If your fund offers more than one contribution option, then you can usually change the amount you are contributing to retirement once a year or more often, depending on your retirement fund rules. You can ask your HR department more about this option. Contributing more will give you a better chance of having enough to live on when you retire from your employer.

You can choose a contribution amount from the options that are provided in the rules of your fund. It is very important to contribute as much as you can every month. You can find out more about your contribution options in your member booklet (which you can get from your HR department).

Your employer might contribute an amount based on your pensionable salary, depending on the rules of your fund. Your pensionable salary (or fund salary) is the part of your salary that your retirement savings contributions are based on.

Yes. The costs of running and administering the retirement fund are taken from contributions. You can find the details of these costs in your member booklet.

If you’re a member of a defined benefit fund, investment performance doesn’t directly affect your retirement fund savings.

Most members belong to defined contribution funds. In a defined contribution fund, the value of investments in your retirement fund’s investment portfolios do affect your retirement savings.

Find out which type of fund you belong to by asking your HR representative or logging onto our website to check your statement.

There are two main things that affect the value of an investment portfolio:

Multi-managers don’t actually buy and sell asset classes, but rather manage the investment managers, who do this on their behalf. Ultimately, multi-managers blend the best assets to give the most appropriate investment management solution. To achieve this they:

A good multi-manager combines the services of selected single managers based on their proven ability in individual areas of expertise, depending on the fund’s particular investment requirements.

Knowing if you’re on track is an important first step to reaching your goals. Use our fun gamified tool to build your retirement picture and find out if you’re on track and what you can do if you’re not on track.